Tax rebates

Tax rebates for residents (individuals):

Individuals who are entitled to use the tax rebates specified in the Law “On Personal Income Tax” - the reduction of the taxable income of a natural person by the donated amounts may not exceed 20% of the earned taxable income. Discounts can be obtained by submitting an annual personal income tax return.

Tax rebates for companies:

Legal entities that are entitled to use the tax rebates specified in the Corporate Income Tax Law (Section 12) may reduce the tax for residents and permanent establishments in three different ways. The donor can choose only one of the following benefits and apply it throughout the reporting year:

-

not to include the amount donated in the taxable base, but not more than in the amount of 5% of the profit of the previous reporting year after the calculated taxes;

not to include the amount donated in the taxable base, but not more than 2% of the total gross salary calculated for employees in the previous reporting year, from which the VSAOI (LV - valsts sociālās apdrošināšanas obligātās iemaksas; ENG - state social insurance contributions) has been made;

to reduce the calculated UIN (LV - Uzņēmumu ienākuma nodoklis; ENG - Corporate income tax) from dividends by 75% of the donated amount, but not exceeding 20% of the calculated UIN from dividends. When choosing type 3 - the amount of donations does not reduce the taxable base, but the UIN from dividends;

Methodological material with descriptions of various situations regarding the application of UIN benefits is available on the VID (LV - valsts ieņēmumu dienests; ENG -

State Revenue Duty) website, as well as cases when the benefits are not applied.

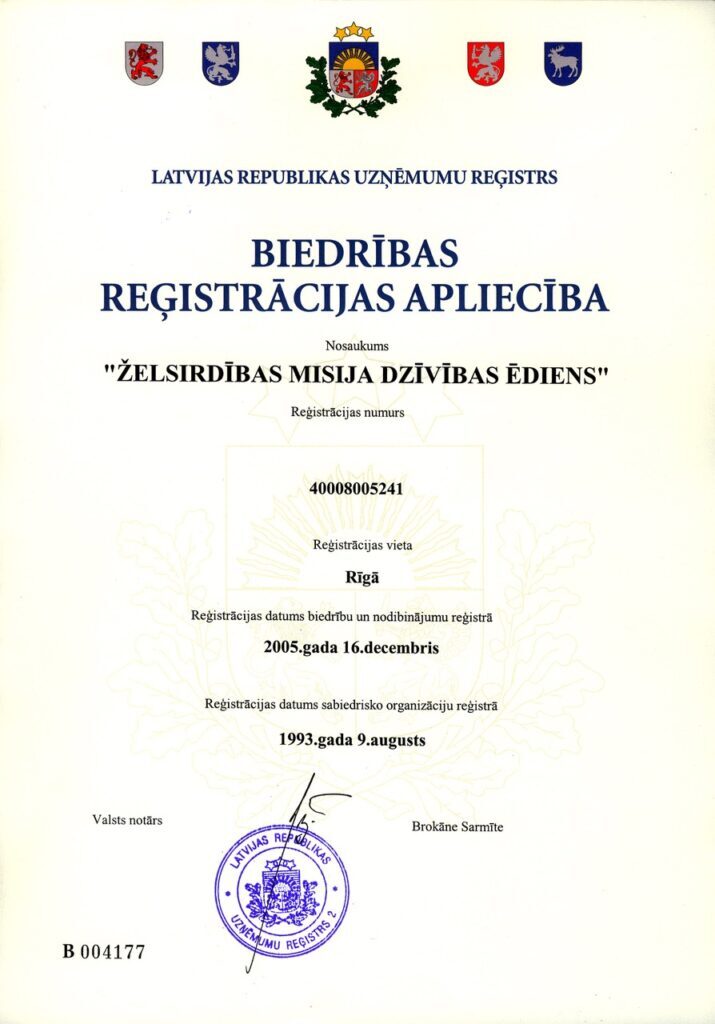

Registration certificate

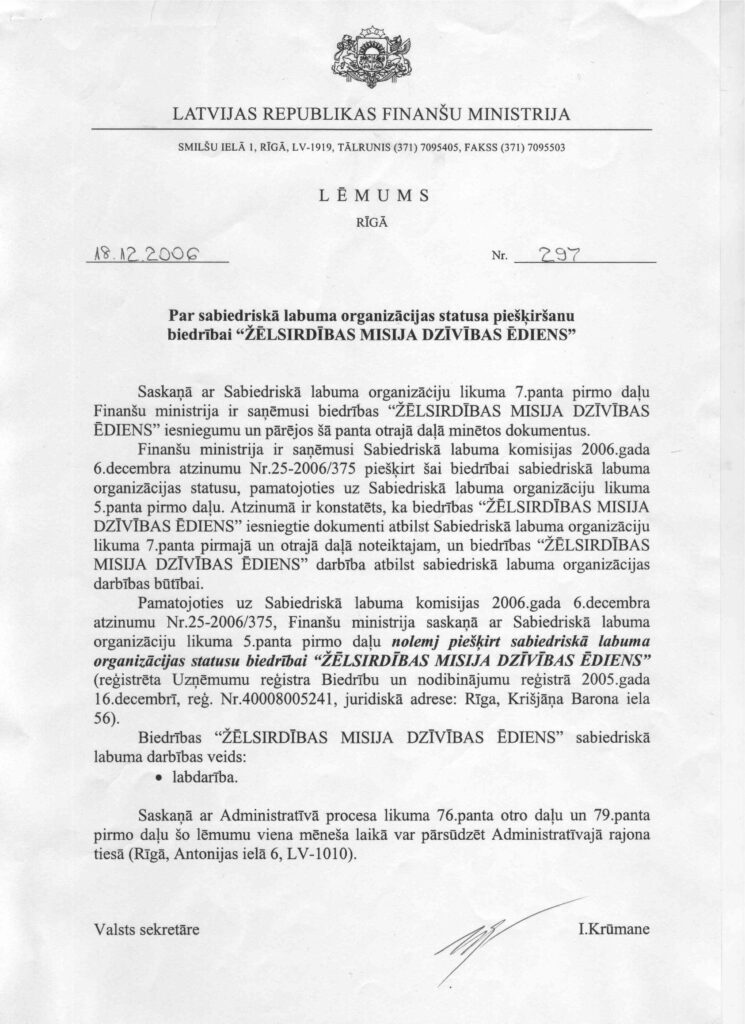

Public benefit status